In today’s age, traditional bonds aren’t attractive to people anymore. Because we now have a lot of other assets and markets to invest in. However, the culprit behind is inflation. It caused bonds to lose their value as the US annual inflation rate takes over the fixed interest rate of bonds. The lower the bond yield, the worse it gets for the investors. Since 1981, the yield on bonds has been declining from 15.8% and the 10-year Treasury yield was lowest at 0.33% in March 2020 and the time of writing is around 3.2%. It is the least risky investment asset, though investing in traditional bonds is considered as a losing game at the moment.

Currently, the crypto market lacks bond investment vehicles or exchanges. Decentralization should be the convenient way to fix the traditional bonds market by introducing solutions for trading, investing, lending, and borrowing of bonds, and it comes up with the D/Bond Protocol, previous DeBond Protocol.

I. What Is D/Bond?

D/Bond Protocol, the pioneer startup building infrastructure for bond and derivative secondary market in DeFi, will also provide frontend and D/Bond wallet, decentralized bond exchange, and an open and functional market for security. The project proposed to operate on the basis that the update of the current yield farming system, which entails maximizing the return on cryptographic assets, will bring more changes, possibilities, and believers to the DeFi system. The outlook will push these financial products and services that are available to anyone that has internet access and can use Ethereum to the next stage where a more complex economic system can be designed using the new bonds token standard.

D/Bond Protocol is striving to be an important player in the decentralization of the derivative and bonds products which has a huge potential in the next generation of DeFi. Aside from enabling users to convert any digital asset to security and getting insurance in repayment, the project promises a more gas-efficient and advanced solution for existing LP tokens. It can make any NFT, LP, and ERC-20 tokens to be convertible into bonds.

The startup will act as a decentralized investment bank that issues bonds for users and provides customized derivatives to hedge against risks. Its income will come from three sectors:

- 10% stamp duty of governance and settlement tokens.

- The service fee for issuing bonds and derivatives contracts.

- The market-making process on secondary bonds and derivatives markets.

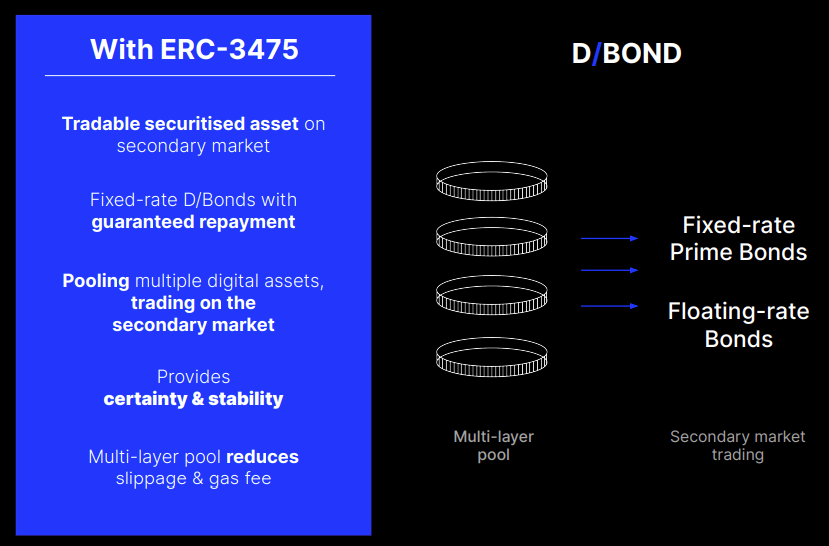

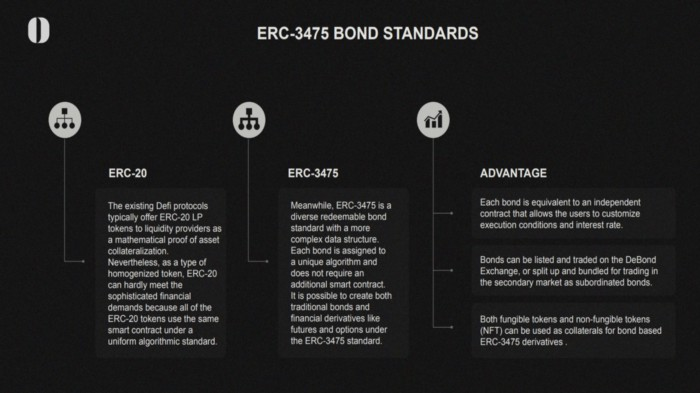

Bonds are new to the crypto marketplace. There are only a handful of projects creating decentralized bond solutions. But the D/Bond project seeks a holistic solution by inventing the ERC-3475 token to represent decentralized bonds.

ERC-3475 Standard

Decentralized bonds count as another asset class that is to be adopted following staking and swaps. Nonetheless, until yet, the respective fixed-rate tools have not performed effectively on the blockchain. The respective interest-bearing securities’ issuance was considered an element of the decentralized finance that none of the protocols could operate efficiently. It is chiefly due to the present token standards not capable of dealing with bonds. ERC-20 is known as one of the fundamental token standards. ERC-20 tokens are utilized on the behalf of a broad range of tokens and are limited in terms of the bonds’ issuance. There is a requirement for ERC-20 tokens to deploy the token contracts for each type of token. The existing ERC-20 standard is incompatible with issuing various classes of bonds. Also, it doesn’t allow storage of some kinds of reward and redemption logic on-chain. This leads to higher gas fees.

Current LP token is a simple ERC-20 token, which has not much complicity in data structure. To allow more complex reward and redemption logic to be built, we need a new LP token standard that can manage multiple bonds, store much more data and is gas efficient. ERC-3475 standard interface allows any tokens on solidity compatible block chains to create its own bond. These bonds and derivatives with the same interface standard can be exchanged in the secondary market. And it allows any third-party wallet applications or exchanges to read the balance and the redemption conditions of these tokens. ERC-3475 bonds and derivatives can also be packed into separate packages. Those packages can in their turn be divided and exchanged in a secondary market.

On the contrary, bonds have particular types and are categorized among diverse classes. D/Bond Protocol in an official announcement on August 25 said the Ethereum Foundation has adopted the EIP-3475 and accepted it as an API standard. Thus, making it possible to issue bonds with multiple redemption data. The proposal has been under evaluation and debate for a long time by the Ethereum Foundation. The ERC-3475 standard will enable anyone to create custom-made bonds on Ethereum. D/Bond Protocol believes the standard will help introduce bonds and add value to the Ethereum infrastructure and ecosystem.

II. How Do Decentralized Bonds Work?

Decentralized bonds are a new and innovative approach for raising funds through the blockchain community. They allow investors to invest money into a new project and yield returns until it is completed. Unlike traditional bonds, DeFi bonds are highly transparent and secure. The idea of allowing investors to earn capital without selling the underlying asset is quite attractive, especially in this uncertain state of the crypto market and global economy.

By issuing bonds, companies borrow money and then pay it back with interest. Of course, the company could take a regular loan, but then it would need to agree on the terms with the bank. As a rule, when it is necessary to raise debt capital, companies more often opt to issue bonds over loans.

For individuals, traders and investors, decentralized bonds are a way to diversify portfolios and take control of risks, since a smart contract guarantees the fulfillment of obligations by the issuer of the bond.

Issuers typically build or develop their own protocol and solutions with the money they raise. Still, they can also invest the money into various other cryptocurrencies, assets, or venture capitals. In addition, bonds are resistant to market fluctuations, so they act as a good hedge in a dicey market.

Decentralized Bonds vs Traditional Bonds

A bond represents debt for companies borrowing money from a third party, with repayments subject to interest payments. However, unlike traditional bonds, a decentralized counterpart is designed to obtain DeFi products with guaranteed liquidity. Through a DeFi decentralized bond, an investor can participate in the success of a company or project without risks. In addition, money is secured for the entire investment period, providing an extra layer of peace of mind. On the other hand, traditional bonds are subject to firms going bankrupt and investors losing their money.

The traditional bond market is an investing area where most don’t meet the criteria. Governments and funds are the only players that can issue bonds. With the emergence of the blockchain and decentralized bond technology, investors and companies will be able to access an open and transparent market that facilitates trade. While traditional bonds are prone to corporate failure and can lose investors their money, decentralized bonds will provide a steady source of payments regardless of market conditions. A key advantage of decentralized bonds is their high liquidity. Investors can expect monthly payments no matter what happens in the financial markets.

D/Bond aims to disrupt this by introducing a P2P bond-securitized loan platform. Anyone is eligible to issue a decentralized bond and use their digital assets as collateral. Users can use a Bored Ape NFT as collateral to get a bond loan. LP tokens represent ownership in a liquidity pool that generates transaction fees. They're like common stock in a bank and are just one of the revolutionary uses of blockchain technology. D/Bond’s collateralization aspect adds more options in decentralized borrowing as there are different types of crypto assets, and investors may favor some over others.

However, despite their risks and costs, decentralized bonds can help unlock the potential for better efficiency and reduced costs in financial trading. It is also worth noting that decentralized bonds let investors earn interest on their wealth without selling assets. Having a pie and eating it is impossible in the current economy, at least where traditional finance is concerned. Hence, the ability to purchase bonds with, as theoretical examples, Bitcoin or Ethereum, and collect monthly payments is appealing. This initiative increases the chance of decentralized bonds getting purchased.

Decentralized Bonds vs DeFi Credit Offering

Term lengths

Current DeFi protocols (Maple, TrueFi) allow borrowers to take out loans with a term limit maximum of 90-180 days. These term limits are too short for an organization looking to use the capital to invest in long term objectives which could take a year or longer to pay for themselves.

For bonds, term lengths are typically on the scale of years, giving borrowers much more flexibility in how the funds can be used.

Loans size

Maple and TrueFi loans are issued out of pools of capital supplied by lenders. This guarantees liquidity for borrowers on the platform but limits the amount of liquidity available to what is in the pool.

With bonds, the maximum amount available to borrow is not limited by the size of a lending protocol’s assets or determined by an underwriter as is done with Maple and TrueFi. Instead, it is determined by the market demand for the debt, allowing strong borrowers to gain more credit than they otherwise would be able to with existing lending protocols.

Collateralization options

TrueFi doesn’t allow borrowers to put up collateral, preventing them from reducing risk to the lender and consequently, their interest rate. On the other hand, Maple allows collateral, but only allows borrowers to put up collateral in WBTC or USDC which may not be favorable for a DAO that wants to use their native token. These problems can be solved by the introduction of bonds to DeFi.

Many collateral options can be provided with the bond sales to reduce investor risk and consequently reduce the borrowing cost. In addition to the aforementioned benefits, which apply to the DAOs issuing the bonds, investors will also benefit from this new opportunity.

III. Market Opportunity

As more governments and companies explore decentralized bonds, the future is bound to get interesting. However, one can’t ignore the potential roadblocks that remain. Decentralized bonds allow anyone to turn a digital asset into a bond. That makes them different from traditional bonds, available mainly to government entities and large-scale corporations. These entities and corporations may not be willing to give up their "exclusive" access to bonds that easily. That said, projects like D/Bond make decentralized bonds accessible today, creating a more level playing field. Users may create their own bonds and derivatives backed by diverse cryptocurrencies such as stablecoins, NFTs or Bitcoin.

A topic to consider is how decentralized bonds may not be suitable for large investments. A fiat bond enables larger amounts to be invested in projects. A decentralized vehicle may not support that option, primarily due to potential liquidity concerns. Even if that issue is resolved, it will still come down to regulation allowing decentralized bonds to gain any traction.

Another rather large outstanding problem can affect the strong development of decentralized bonds, that is a legal issue. The cryptocurrency market does not have enough legal basis and corridor to ensure the safety and ability to borrow capital from companies, organizations or startups.

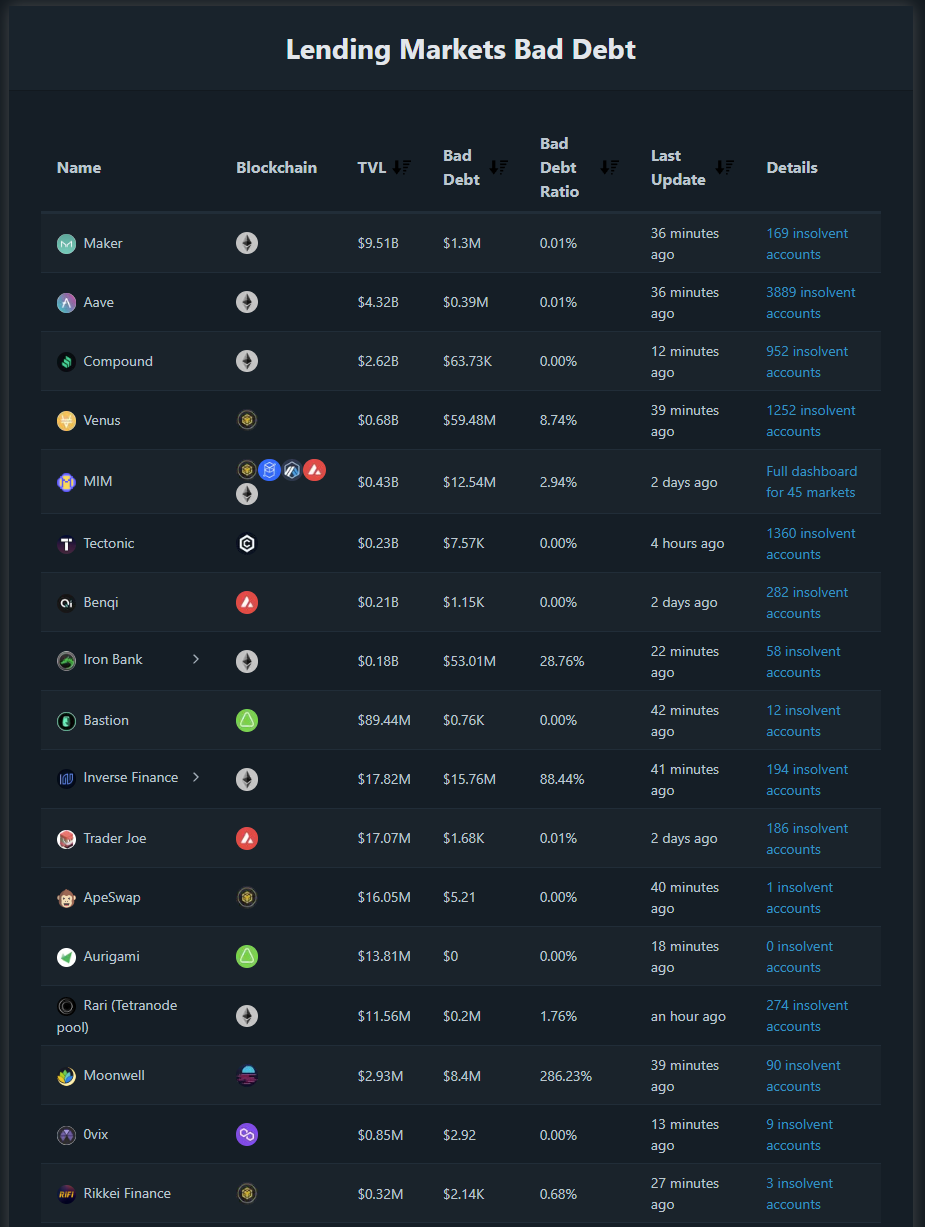

Source: RiskDAO.

Ignoring macro issues aside, the potential for decentralized bonds to be listed in DeFi's categories is large enough. Let’s do some math, there are about $10T of US corporate bonds outstanding as of 2Q 2021 and the total market cap of US public companies is roughly $50T. Let’s assume the total US corporate market cap of public and private companies is $100T a rough assumption but necessary to estimate the decentralized bond market size, might be one fifteenth as of Total Value Locked in DeFi which the all-time-high value was once over $180B.

IV. Tokenomics

The D/Bond Protocol consists of two types of tokens: DBit (Decentralized Bonds Index Token) and DGov (Decentralized Bond Governance Token).

DBIT represents an un-capped supply token that acts as the utility token for the protocol, acting as the market settlement currency. All the interest from the primary and secondary markets will be transferred through. DGOV is the limited supply governance tokens for allowing holders to add proposals in the D/Bond governance for protocol upgradation and decisions related to the treasury, as well as participating in the voting process by staking.

A valuation at $12.5M with $500k fund raised from Seed round, token price pegged at $25. The announcement of a Private B round that entailed the sale of 130,000 tokens intended to raise more $4.5M just increased the new valuation by 40% at $17.5M and price of $35. It can be said that the valuation in the latest round of funding of $17.5M is acceptable for the idea. Considering the market size and market share of the bond sector in the current DeFi industry that the project can achieve in the future, there would be a lot of room for growth.

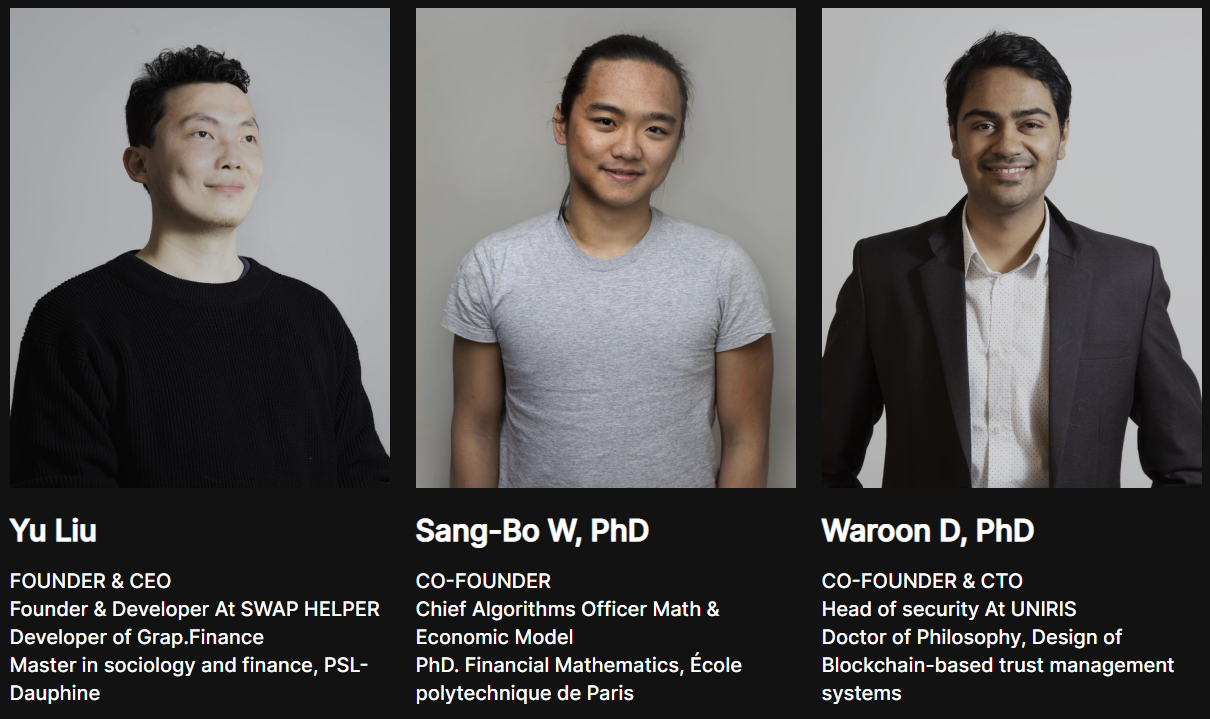

V. Team & Partners

Introduced with quite potential staff and good background, with 12 dedicated experts, 6 nationalities, 6 engineers, 5 PhDs and PhD candidates. Founders had over three years of experience and products related to blockchain and DeFi, but those projects were not maintained and completed. But with the records of their profiles and the vision to grab the big piece of DeFi's cake from the untapped bond market is completely ambitious.

VI. An Initiative For A New DeFi 2.0 Chapter

The bond market is an area DeFi has missed, and soon, we’ll see how DeFi manages to disrupt and evolve it. So far, DeFi has already proven to create lucrative opportunities out of traditional finance features. A decentralized bond market is designed to stabilize the volatile crypto ecosystem. Moreover, the ERC-3475 standard will transform DeFi and Web 3.0 and further boost their adoption. Ultimately, bonds on DeFi will be the next innovative asset class on DeFi after swaps and staking.