Derivatives trading on-chain has really taken off, with big players like GMX seeing $166 billion in total volume, and Vertex Protocol not far behind at $72 billion. These numbers are still climbing, especially now that the market is on an upswing.

Given this momentum, it’s no surprise that the idea of copy trading or managing assets on-chain is getting a lot of attention. However, not every platform aiming to innovate in this space has hit its mark or made a significant impact. Let’s look at some examples to see why they might not have reached their goals.

I. Unsuccessful cases

Just like startups in Web2, Web3 projects face similar, if not greater, risks and uncertainties. The expectations of Web3 users are often much higher than those of Web2 users, adding much to the challenges. There's no guaranteed recipe for success in this innovative yet volatile space. Several critical factors play into the success or failure of a project - market conditions, the product itself, marketing strategies, foundational theories, or sometimes, even a misstep as minor as an intern's social media post can tip the scales. Now, let's look into a few examples of projects that, from our perspective, didn't hit their targets.

Solana Asset Management platforms

There were several Asset Management Platforms/Copytrade options on Solana, with Solrise being the biggest name among them. They launched their product in 2021 but had to shut down in 2022 after things on Solana took a downturn.

To get a sense of what happened, it’s helpful to check their social media: SolriseFinance Twitter.

Solrise didn’t hold onto liquidity themselves but instead outsourced it to other protocols on Solana: Jupiter and Mango Market. They focused on bringing KOLs/Traders onto their platform.

However, their Achilles' heel was the limited number of trading pairs available on Mango Market and Jupiter, which remains minimal to this day. They couldn't compete with even the smaller CEXs, let alone giants like Binance, Bybit, or OKX. It's unrealistic to expect traders to flock to a platform that only offers BTC, ETH, and SOL for trading.

Another critical issue was Solana's instability at the time. Conducting Perpetual Trading on a blockchain that experienced downtime 10 times a year was too risky. The collapse of FTX only added to their troubles.

Despite these challenges, Solrise did identify important focal points: Traders and Community. Props to them for that.

dHedge

dHedge stands out significantly in the Web3 Asset Management space, potentially being one of the biggest names here.

Having raised over $12 million from some reputable names, they remain active to this day. dHedge prioritizes Autonomous Strategies and various DeFi activities, targeting Western hedge funds interested in developing automatic strategies.

From the perspective of the VCs who invested in them, dHedge hasn't lived up to expectations. Despite raising $12 million, their TVL is around $40 million - a figure that dipped to $10-20 million during the bear market - and their trading volume hasn’t been particularly impressive. This has led to perceptions of the asset management market being bearish.

However, it's important to remember the story of Axie Infinity, which didn’t take off immediately in 2019 and even into 2020.

One of the reasons dHedge hasn't captured widespread interest is that it wasn't designed for the average investor. It’s created for institutions looking to dip into crypto markets with reliable yields and income, rather than for the general public. For everyday investors, a 5-7% yield through Stablecoin Liquidity Pools isn't attractive, especially when they have the option to manage their investments themselves.

Yet, as institutional interest in the crypto market grows, these entities might opt to either develop similar platforms on their own or turn to dHedge. Protocols similar to EthenaFi/Delta Neutral Strategies could be implemented on dHedge. The interest simply hasn't been strong enough yet, but that doesn't mean it won't be in the future.

However, it must be acknowledged that dHedge’s tokenomics were not particularly well thought out, and launching during a DeFi bear market certainly didn't help their cause.

Nested.Fi and Valio.XYZ

Nested.Fi and Valio.XYZ are grouped together here due to their noticeable similarities. Both platforms are designed as copy trading tools, created by individuals who are not traders themselves and struggling to pinpoint a unique selling proposition (USP). Nested.Fi has gone through a rebranding to Mass.Money, while Valio.XYZ has not been generating significant trading volumes.

The design of these platforms does not seem to attract serious traders or investors, perhaps with the exception of a Gen Z audience.

It’s essential to understand the difference between Copy Trading and Asset Management, as they might seem similar but are quite distinct. Web3 Copy Trading involves finding an individual or institution whose performance or investment thesis you admire and attempting to replicate their strategy. On the other hand, Asset Management involves entrusting your funds to a third party. Profits are shared, but management fees are involved. Comparing Web3 Copy Trading with Asset Management could be the same as the difference between pirating music/movies and paying for them. Copying someone without their permission offers no incentive to the original strategist. Without incentives, such practices can be easily exploited, especially by whales and high-net-worth individuals who are increasingly aware of on-chain tracking. They might think, “Why should we let these freeloaders benefit from our strategies?” and take actions that could render the most closely watched wallets ineffective or use them as tools for market manipulation.

Meanwhile, Asset Management provides Asset Managers the incentives and rewards to manage assets for other users. New Creator Economy. But in the case of Valio, what kind of incentives are they actually receiving? Are we talking about 1-2% of Assets Under Management (AUM)? Or perhaps 10% of the profits made on those AUMs?

Consider a scenario where Manager A's AUM is $1 million, and they achieve a 20% Return On Investment (ROI), a standard figure in the industry. This means, after a year, they would earn between $20,000 to $40,000 USD. This calculation stands only if they indeed manage an AUM of $1 million, which is a figure even the platforms themselves struggle to reach in total.

Why don't these platforms have significant AUMs? The simple answer is the lack of users. They struggle with marketing to the right audience—those who are willing to entrust their funds for passive income. Moreover, they find it challenging to attract skilled traders or KOLs to the platform since the only incentives available are marketing fees. In Web3, the mantra often is: no token, no fun. Tokens are vital for aligning the incentives of individuals and the community that contribute to building everything. Yet, these platforms have secured investments from VCs, who are unlikely to favor diluting their investments by distributing tokens freely to every user online.

And another point to consider: one year is a long time in crypto, at least as things stand currently. Few traders are interested in committing to a platform for a full year just for a $20,000 paycheck—except maybe those hunting for airdrops.

However, there are other notable names in this space worth mentioning and learning from, including STFX, Hyperliquid, and Ox.Fun. It's likely there are more projects in the pipeline that aren't on the radar yet, along with others that are set to launch. This signals a highly competitive environment in the near future for this sector.

II. The Rising Stars

STFX

It’s important to acknowledge STFX, as their thesis on "The Vaultification of Everything" has been particularly inspiring. They argue for a unique approach to structuring crypto investments, which you can look into through their detailed exploration on Medium and The Mothership's insightful analysis.

STFX states that given the typically short attention span of crypto traders, each DeFi Vault should focus on a single position. While there's strong disagreement with this perspective, it’s undeniable that STFX stands out for its execution among the platforms discussed, achieving better volume accumulation. Yet, there’s a strong belief that Berally could match or surpass STFX’s accumulated volume in just one month, as opposed to a year.

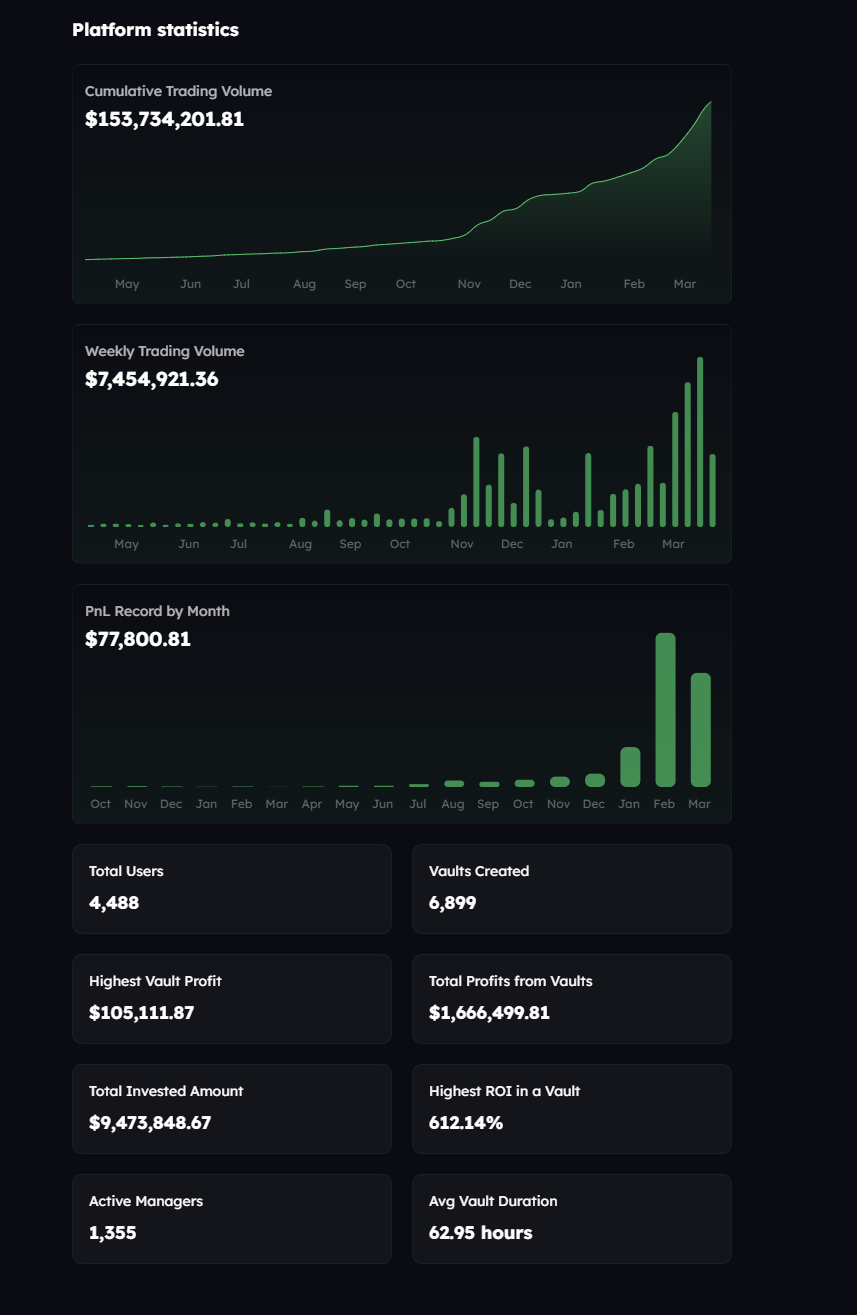

This shows two crucial points. First, the importance of social trading and co-investing. Second, take a look at their statistics:

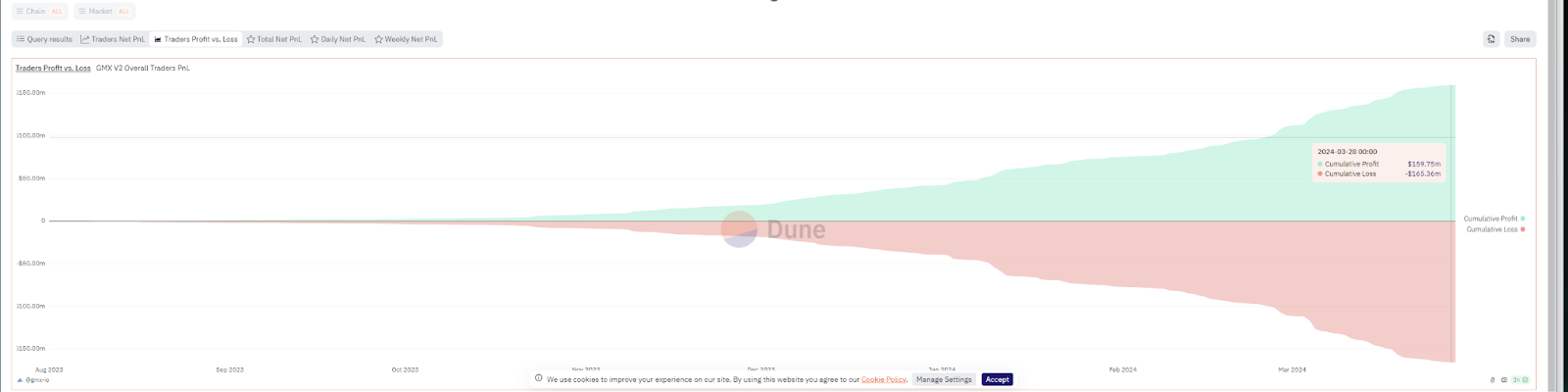

Now, compare to the situation with GMX Traders on Dune:

It revealed one key concept: Specialization. The specialization of the labor force is fundamental. Just as you wouldn't seek a professional athlete's assistance during a medical emergency but rather a doctor's, it's unreasonable to expect everyday people to trade as proficiently as professional traders.

The concept of co-investing or social trading has been recognized for its potential to generate profits for retail investors over the long term, and many are well aware of this. That's precisely why the demand for such services on CEXs is continuously growing. Look at platforms like OKX, Binance, or Bybit. Even eToro is generating more profit than most of the top 100 companies listed on CoinMarketCap. This begs the question: Why not implement social trading on the blockchain? Further thoughts on this topic have been shared by our CEO here: Tweet by @cuongdo_cl.

Despite the innovative approach of STFX, it's noteworthy that their volume, along with profit and revenue, remains low. This level of performance is particularly concerning for exchanges. With this in perspective, it's worth turning attention to Hyper Liquid to understand their strategy and operations.

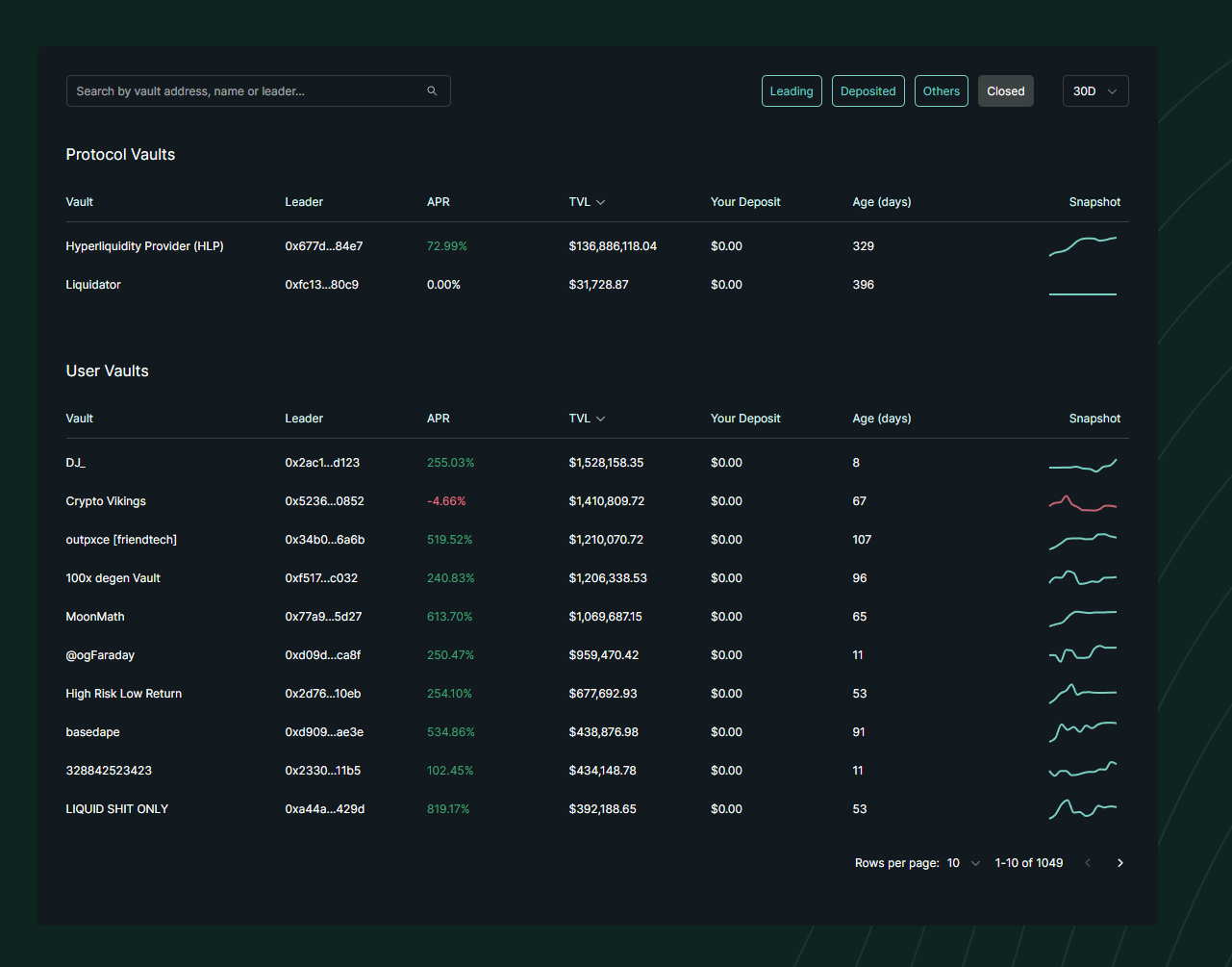

Hyperliquid

The standout core of Hyper Liquid compared to other platforms discussed is their ownership model: they own the blockchain, the infrastructure, the liquidity, and they've implemented social trading through User Vaults. This comprehensive control contributes to their superior volume, TVL, and other metrics. The driving force behind this success? Incentives.

It cannot be emphasized enough: In Web3, incentives are key. What accelerates the pace of Web3 startups beyond that of Web2 companies is the distribution of incentives for contributors. Programs rewarding points have proven to be a significant motivator, overshadowing other factors like user UI, speed, and additional features, which are merely bonuses. It's the incentive programs that attract and retain traders.

Hyper Liquid recognizes this, adopting strategies similar to those of the top CEXs, and their success speaks for itself. However, this success brings to light a crucial question regarding their future: what happens to HyperLiquid's user base once the incentive programs, like point systems and airdrops, stop? Will traders remain loyal, or will they migrate to other platforms in search of new incentives?

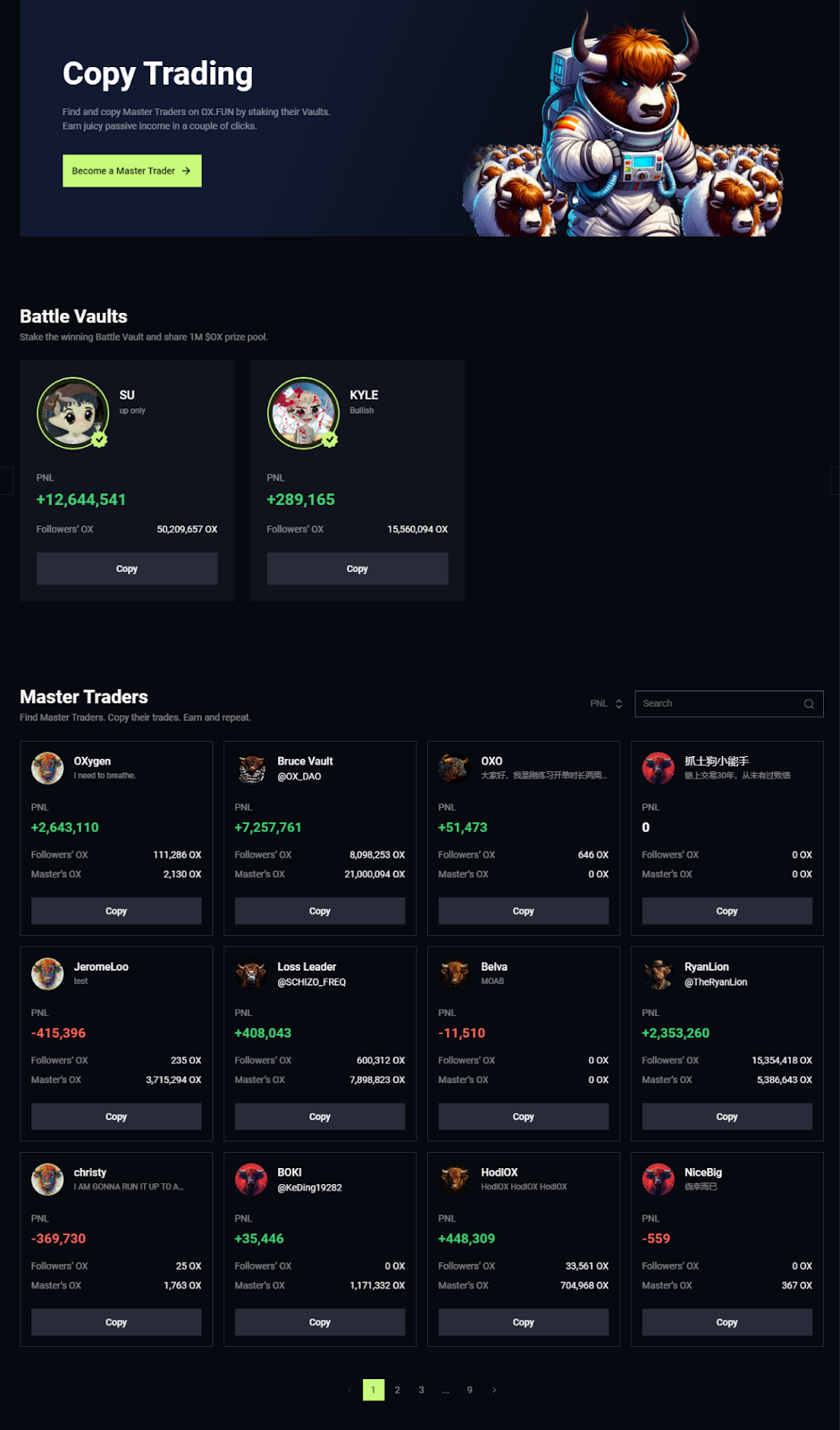

Ox.Fun

Ox.Fun stands out, particularly for its marketing strategy, which is perhaps not surprising given the backing of notable figures like Suzhu and Kyle (3AC Capital founders). It's essentially the on-chain iteration of the Oxbull Exchange, which was shut down a few months ago. However, making a bold comeback, they've decided to distribute their tokens directly to Master Traders.

The revenue model is straightforward yet clever: earnings come from the trading fees and the circulation of OX tokens. This setup creates a self-sustaining cycle where users purchase OX tokens, stake them to earn profits, and, in turn, contribute to the platform's revenue through fees and token purchases. The profits are then distributed to Master Traders, who attract more followers to the platform, enhancing its growth and activity.

III. Berally by Chainslab?

This article has walked through Berally’s approach and structure. If you’ve read up to this point, we appreciate your time. In a market where many investors and platforms are looking for quick results, Berally is focused on the broader shift, particularly the move toward on-chain platforms.

The key questions remain: What makes Berally different? And what are the realistic chances of capturing a piece of this emerging market?

Berally’s platform is built around more than just friendtech and dHedge. It integrates social engagement with everything on-chain, aiming to create an environment where traders can interact and manage assets for others. The idea is that this social component may attract more participation from traders and retail investors, potentially increasing the platform’s activity.

The Social Layer

If you followed platforms like Friendtech in 2023 or Bitclout in 2021, Berally’s Social Layer might sound familiar. The Pass mechanism allows users to buy social tokens of other players in the protocol. Typically, the earlier someone buys in, the better the deal they get. There has been some criticism about these kinds of systems, with some suggesting they resemble Ponzi schemes, where KOLs might exploit their followers. It’s true that many economic models, whether in real estate or infrastructure, rely on continued participation to maintain growth.

The important distinction between different systems is the value they provide. Some models generate real utility, while others don’t. For example, Berally’s Pass mechanism offers specific benefits to holders, like potential profits, beyond just access to a chat or a group.

Additionally, the Pass curve offers users the flexibility to control how the price evolves over time, allowing for different strategies and giving users more control over their participation.

The DeFi Layer

Simply put, Pot is a DeFi vault designed to enable users to conduct various on-chain activities together.

Some people compare Pot to Hyperliquid vaults, which makes sense as a current market analogy. However, Pot is built to support a broader range of uses. Through complex technical setups and integration with SAFE, Berally can incorporate virtually any on-chain project into Pot. This means it goes beyond just perpetual trading, covering activities like spot trading, yield farming, and even on-chain gambling.

Moreover, Berally’s user interface integrates with other protocols, so users can interact with these features without needing to navigate unfamiliar systems or buttons. It aims to simplify the on-chain experience while offering a wide array of DeFi tools.

Sounds like unreal just like Berachain, right?

IV. Conclusion

As we've explored, Web3 asset management and social trading have been through the ups and downs. While several platforms have attempted to carve out their space, each has faced its own set of challenges, whether due to market conditions, platform limitations, or user expectations. Projects like Solrise, dHedge, and Nested.Fi have demonstrated the difficulties of achieving broad success, particularly when trying to balance utility, market fit, and user engagement.

Berally is built from hard-earned lessons, and it’s built by people who eat, sleep, and breathe this stuff. Will we make it? Who knows, honestly. Berally might just be a stepping stone, a lesson for the next SocialFi project to truly take off. Or maybe, just maybe, we’ll be the ones who find that product market fit right after Friendtech’s collapse. Either way, we’re here for the ride, and we’re all in.